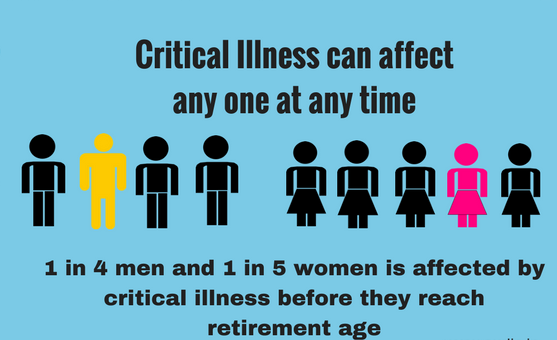

One of the most frequently talked about insurance type is Critical Illness. Most of us own a Term Life Insurance and Health Insurance. However, we never comprehend the importance of having a Critical Illness policy. You might have heard about this policy from either your Insurance agent, or from friends who have purchased these policies. But what does critical illness cover?

A Critical Illness cover is a type of insurance that pays out a lump sum amount to a policy holder when an individual is diagnosed with an illness that is covered under the policy. The money is tax-free and can be utilized in any manner that you prefer – be it to pay a lump sum off your mortgage, to buy private medical care or a fund you’d like to keep for you to stop working.

How does a Critical Illness plan work?

A critical illness cover is different to that of a mediclaim. A critical illness cover provides a lump sum benefit which can be utilized for paying the cost of care for a treatment, or any recuperation expenses. Therefore, critical illness policies are defined-benefit plans since the payout is demarcated and fixed. On the other hand, a mediclaim is an indemnity plan which gives the reimbursement amount basis the expenses incurred.

Every critical illness plan covers a listed set of illnesses. If you encounter any of the stated illnesses which are covered by the plan, only then you are entitled to the benefit. The benefit is given solely on the basis of diagnosis of any covered illness. It’s up to the policy holder whether to seek treatment for the same or not. Besides this, the policy holder should survive for a 30-60 days post diagnosis of the illness in order to avail the benefit of the policy.

How to choose a suitable Critical Illness plan?

Coverage size

There’s no specific yardstick as to how much cover is right. But ideally, it shouldn’t be any less than Rs. 10 lakh. Also, a few experts suggest that it should be 4-5 times of your annual income. If you feel you’re capable of paying a higher premium, then you should opt for a higher cover. This will support your future medical inflation for a certain time frame.

Renewal option

While picking a plan, always opt for the ones that provide with lifelong renewable option. As you grow older, the possibility of facing critical illness increases, and hence you need a policy that offers you the lifelong renewability.

Illness covered

The number of illnesses covered under the policy varies with different insurers. Most of the policies cover about 8 to 20 major critical illnesses or sometimes even more. Some of these are major cancers, heart attack, kidney failure, stroke, loss of speech, coma, major organ transplant, major burns and paralysis. The coverage amount is anywhere from Rs. 1 lakh onwards.

Premium amount

The higher cover you will look for, the higher premium you will have to pay. Nothing is at free. Hence, it is important to understand your financial capacity and requirements and then plan accordingly. The premium increases as you grow older. However, if you have taken a critical illness plan as a rider with Life Insurance, then the premium remains the same throughout the policy period.

Claim Settlement Ratio

Even though it’s rare to find the exact reasons behind the rejection of the claim, understanding the claim settlement ratio of your insurer could give you an indication of how the company performs when it comes to dealing with claims.

Critical illnesses come with a considerable price tag attached and critical illness plans or rider helps in such cases. So it’s important to understand how these plans function and accordingly buy one for an enhanced protection against those deadly diseases.